BRICS vs G7: The Battle for Global Economic Power

Explore how the BRICS nations are challenging the G7’s dominance in 2025. Learn the key growth drivers, risks and what this means for investors in global markets. BRICS vs G7, BRICS 2025 economy, G7 economic power, global economy 2025, emerging markets growth

11/2/20254 min read

1. Introduction

In the shifting landscape of the global economy, two major blocs stand on opposite sides of the balance: the advanced‐economy grouping Group of Seven (G7) and the emerging‐market coalition BRICS (Brazil, Russia, India, China, South Africa, plus recent expansions). The question for investors, policy‑makers and market watchers in 2025 is: Which bloc will steer the future of global economic power?

While the G7 maintains deep institutional advantages, the BRICS nations are growing at a faster pace, leveraging demographics, natural resources and emerging market dynamics. This article analyses the current standings, the drivers, the risks and what this shift means for global markets and your portfolio.

2. Where Things Stand in 2025

Economic Size & Growth

The G7 bloc comprises seven of the most advanced economies in the world. Its combined nominal GDP remains dominant, though growth has slowed. According to one source, the G7 combined nominal GDP in 2024 was around ~US$45 trillion, representing roughly 45 % of global GDP. VarIndia+2Voronoi App+2

The BRICS nations in comparison generated about US$27–30 trillion in nominal GDP, equivalent to ~25‑30 % of global output in recent years. CryptoRank+2Visual Capitalist+2

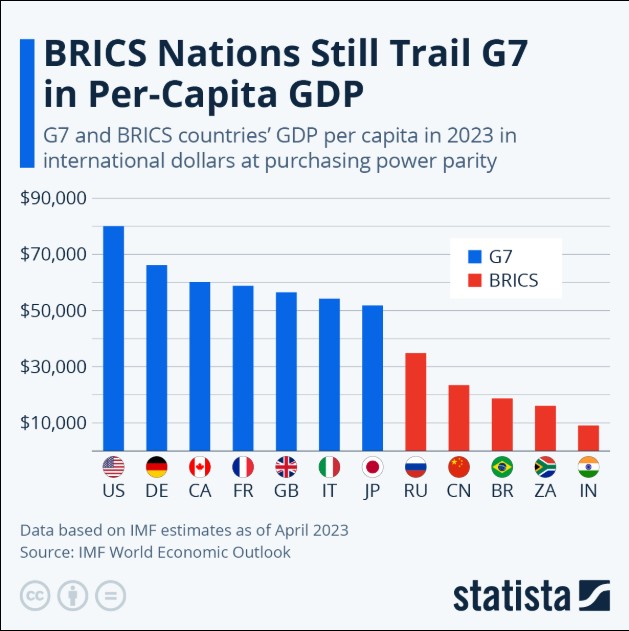

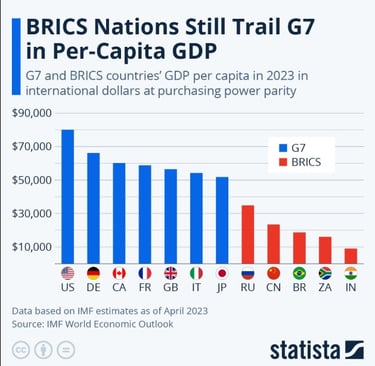

In purchasing power parity (PPP) terms, the gap narrows — BRICS may account for ~35‑40 % of world output, while the G7 share may be in the high‑20s. BRICS+1

Growth projections show a clear dichotomy: BRICS nations are expected to grow at ~3.4‑4 % or more in 2025, while the G7 may grow at ~1.0‑1.5 %. CPG Click Petróleo e Gás+1

3. Key Growth Drivers for BRICS

Demographics & Resource Endowment

BRICS countries — particularly China and India — benefit from large populations and expanding middle‑classes. This translates into growing domestic markets, new consumption patterns and greater investment potential. Combine that with rich natural resources (minerals, energy, agriculture) and you have a potent growth cocktail.

Reform & Infrastructure

Many BRICS nations are investing heavily in infrastructure, manufacturing and technology to leap‑frog older development models. These investments boost productivity and can underpin faster growth than mature economies.

Shifting Global Trade & Production Chains

As global supply chains restructure (due to geopolitics, pandemic effects, technology), the BRICS bloc is well‑positioned to capture manufacturing, processing and export growth. Coupled with trade partnerships among themselves and with other emerging regions, they are building an alternative axis of commerce.

Financial & Currency Diversification

Some BRICS countries are moving to reduce reliance on Western financial infrastructures (e.g., Western‑dominated reserve currencies, payment systems). This drives policy shifts, including increased gold reserves and regional payment mechanisms. golden-mart.com

4. Strengths Still Held by the G7

Institutional Depth & Innovation

The G7 economies benefit from mature institutions, deep financial markets, advanced technology sectors and strong rule‑of‑law frameworks. These features translate into stability, predictable investment environments and leadership in global standards.

Per‑Capita Income & Wealth

Although the BRICS in aggregate are large, the per‑capita GDP of G7 members remains far higher, which means more consumption power per person, better human capital and more innovation.

Global Financial Architecture

The G7 bloc retains significant influence through international institutions, reserve currency privileges (especially the US dollar), and global banking/settlement networks. These advantages are not easily eroded overnight.

5. The Risks & Challenges Face Both Blocs

For BRICS

Internal cohesion: BRICS is a diverse group (geographically, politically, economically). Fragmentation or conflicting interests could undermine collective strength.

Structural challenges: Lower per‑capita incomes, governance issues, resource dependency, and weaker institutions in many BRICS countries.

External shocks: Vulnerability to commodity price swings, geopolitical conflict, currency risks, and capital flight.

For G7

Slow growth & aging populations: Many G7 nations face demographic headwinds and low productivity growth.

Debt burdens & fiscal constraints: High public debt limits room for policy manoeuvre.

Erosion of dominance: As BRICS rise, the relative position of G7 could decline, possibly reducing its leverage in global governance.

6. Implications for Investors & Global Markets

Geographic & Sector Shifts

Emerging markets exposure: With BRICS growth outpacing G7, investors may consider increasing allocation to emerging markets, resources, and consumer sectors in Asia/Africa.

Alternative asset themes: Resources, infrastructure, regional trade corridors, and local‑currency assets in BRICS regions may gain more prominence.

Diversification of risk: As power shifts, currency risk, geopolitical risk and supply‑chain risk become more salient—investors should adjust hedge strategies accordingly.

Strategic Asset Allocation

In G7 markets, the value may increasingly lie in innovation, services, and high‑end manufacturing.

In BRICS markets, volume growth, consumption upgrades, infrastructure investment and “catch‑up” dynamics could drive returns—but with higher risk.

Considering the gap in per‑capita incomes, there may still be value in G7 stable assets, especially for risk‑averse portfolios.

Currency & Reserve Dynamics

As BRICS build their economic clout, we may see shifts in reserve currency mix, bilateral trade settlement currencies and investment flows. This can affect exchange rates, bond markets and global liquidity.

7. What to Watch in the Coming Years

Membership expansion: BRICS may continue to broaden its membership, further increasing its economic weight and geopolitical influence. BRICS+1

Technological leap‑frogging: Whether BRICS nations can successfully move up the value chain into advanced manufacturing, innovation and services.

Global governance reforms: Changes in institutions like the IMF, World Bank and global trade norms, which could shift power away from Western‑led frameworks.

Macro shocks: Inflation, energy transitions, climate policy and geopolitical conflict can alter growth trajectories for both blocs.

8. Conclusion

The contest between the G7 and BRICS is not just about size—it’s about the trajectory of growth, structural resilience and future influence. As of 2025:

The G7 still commands institutional strength, higher incomes and global financial dominance.

The BRICS bloc is growing faster, representing a substantial share of global output and gaining momentum.

For investors and market participants, that means balancing stability with growth. A strategy that blends exposure to the mature G7 economies with dynamic BRICS growth stories may provide optimal tilt for the decade ahead.

When power gradually shifts, the early mover may gain greater gains—and the early analyst may craft better outcomes.